Of all the reasonably well-intentioned but ultimately misguided deductions which deliver the vast bulk of their benefit to the well-off (and very well-off), the king is the mortgage interest deduction (or MID). It’s got to go.

According to noted pinko rag The Economist:

The MID is almost impossible to defend on distributional grounds. It only goes to people whose income is high enough to merit itemising deductions, and its value rises with their tax bracket.

A study for the Urban Institute and Tax Policy Center by Eric Toder, Margery Austin Turner, Katherine Lim and Liza Getsinger estimates that its elimination would cost the average household an average of $559 more per year in tax. But the impact is highly progressive: for bottom quintile the average increase would be just $2 or 0.01% of after tax income; for the middle quintile, $215 or 0.49% of income; and for those in the top quintile minus the very richest 1%, it would average $1,723 to $4,234, or 1.59% to 1.63%. Only for the richest 1% does its relative importance decline.

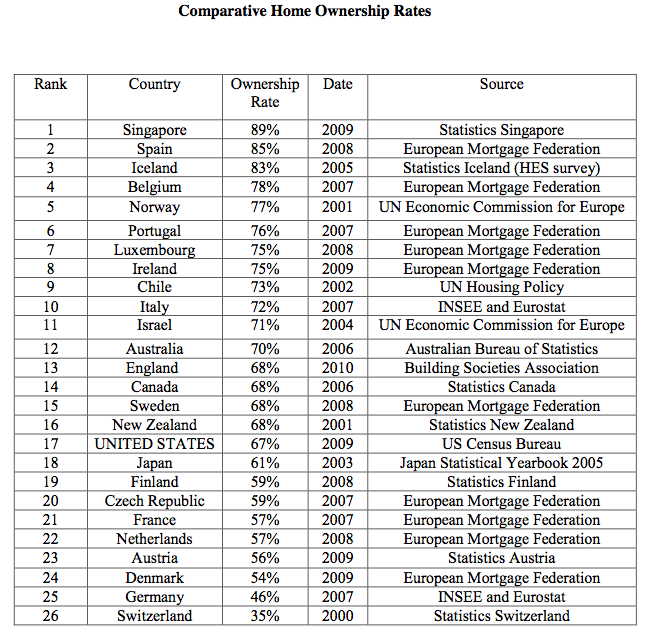

The study notes that the MID has not been found to increase home ownership, which makes intuitive sense: the families that benefit are precisely those most able and likely to buy a home regardless of the tax treatment. It only encourages them to buy larger homes, and to do so with more debt; anyone who pays off their mortgage gets no benefit.

So how did we end up with an expensive program – about $100 billion a year -- that does pretty much nothing to boost home ownership rates, but offers yet another way for the well-off to save more money.

|

| From the testimony of Alex Pollack before the Senate Committee on Banking, Housing and Urban Affairs |

According to Roger Lowenstein* of the New YorkTimes, the idea of a mortgage for a home is a relatively new idea. Until the 1920s, homes were typically paid for in cash, although farms would be purchased with the help of a mortgage. As such, it made sense to allow a deduction for mortgage interest, as the farm was the family’s business.

In fact, no one paid much attention to personal interest deductions at all until 1986. By then, credit cards had become a staple of modern life, people were accruing more and more debt, and they were deducting the interest on that debt from their taxes. The Tax Reform Act changed that, but did preserve a deduction for mortgage interest – the first time such a distinction had been made. (This legislation also taxed capital gains as ordinary income, a point we discussed here.)

So why doesn’t the mortgage interest deduction help home ownership?

Imagine a world with no mortgage interest deductions (by the way, this place exists – most other countries don’t offer this deduction) where you’re looking to buy a home and you’ve got a budget of $225,000. Fortunately, there is a nice house available at that price point. But there’s a really nice home available for $250,000, but that’s just too far over budget for you.

You wake up the next day to find that the mortgage interest is now deductible, so you re-calculate your housing budget and learn that $250,000 is now doable. You call up your broker to place a bid, but he tells you that $250,000 will no longer do it – the asking price is up to $285,000. But he does have a nice home available for $250,000 – it’s just the same one that cost $225,000 the day before.

This is because when Congress made mortgage interest deductible, they made it deductible for everyone. So everyone at a given budget point X got an identically sized gift Y to spend on a house. You're still competing with everyone else with an X budget, you're just competing with more money -- (X + Y).

So who wins in this situation?

Well, firstly, the realtors win. Realtors work off commissions, so anything which increases the prices of homes is good news to them. Secondly, the banks win, and for the same reason. When a home’s value increases, that means the bank can write a bigger mortgage on that property, and collect more interest. And the well-off win, for several different reasons.

Melissa Labant, technical manager at the American Institute of Certified Public Accountants, calculated two situations for middle- and upper-income homeowners in more expensive states.

In the first situation, consider a couple who earn $137,300 a year and are in the 25 percent tax bracket. If they owned a $350,000 house paying 5 percent interest on their mortgage, they would save $4,375 a year on interest of about $17,500.

For the wealthiest homeowners the deduction is far better. People with $1 million homes with the same 5 percent rate would be paying $50,000 a year in interest. As they would most likely be in the top 35 percent tax bracket, they would save $17,500 a year in federal taxes through the deduction.

As the well off have bigger mortgages, they’re able to deduct more interest. But the well-off may well have more than one mortgage – and the mortgage interest deduction applies there, too. So we end up subsidizing not only home ownership, but vacation home ownership as well – which seems a bit much. In fact, all mortgage interest is deductible up to $1 milliona year. Who the hell has $1 million a year in interest payments?

Finally, not only is mortgage interest deductible, but so are the interest payments on home equity loans. As home equity loans actually require you to already own a home, they do little to increase home ownership.

(One of the tricks in the securities industry was to take the proceeds from a low-interest home equity loan and use it to fund a securities trading account. If a margin account were used instead, the interest payments would be higher, and they wouldn’t be tax deductible.)

Unfortunately, the mortgage interest deduction is often viewed as one of the several third rails of politics. But recent polling suggests that Americans may be ready for a change.

Now, according to a recent Bloomberg Poll, a growing number of Americans may be willing to end the mortgage tax deduction -- as long as they get something in return. Forty-eight percent of respondents said they were willing to give up all tax deductions, including the home mortgage deduction, in return for lower tax rates for every tax bracket. Forty-five percent were opposed in the survey of 997 adults.

So now that we’re all on board for killing the MID, how do we do it? Unfortunately, we can’t just do it all at once. Many people purchased homes with the expectation that their mortgage interest would be deducted, and they may not be able to afford those homes without it. But we can take care of the most egregious parts. We can eliminate the tax deduction as it applies to new home equity loans, which shouldn’t be much of a problem; banks aren’t making many of these loans anyways. And we can similarly eliminate the tax deduction for anything but primary residences – gone are the subsidies for beach houses (unless you actually live on a beach).

And we can address the primary deduction gradually. As noted earlier, the maximum allowable interest is $1 million a year. If we reduced the cap by $200,000 a year, we wouldn’t affect anyone but the screamingly well off for four years. And as for the fifth year, we would be fine if we cut the tax rates for the poor and middle class, so as to compensate for the (minimal) effects of ditching the mortgage interest deduction.

And without the mortgage interest deduction, we've actually made preparing your taxes easier. Now even more people will take advantage of the standard deduction. You're welcome!

* Roger Lowenstein – who penned the best article on Social Security we know of – also wrote the best article on the mortgage interest deduction, which has been added to the Reading List sidebar. If you want to know more than your neighbors, that’s the place to go, and that’s where most of the following information came from.

No comments:

Post a Comment